Why FWF Market Insights?

FWF’s market analysis provides up-to-date transportation industry insights and trends, enabling you to navigate a constantly moving logistics industry. Understanding the fundamentals of how rates are affected and monitoring new trends begins with understanding supply and demand. It is vital for your business planning and market knowledge.

If you want to learn more, check out FWF’s Basic Breakdown of Supply and Demand.

Overview

The beginning of the first quarter of 2022 began much differently than how it ended. Spot rates remained elevated as the tight capacity of the 2021 freight market followed into the new year. As capacity constraints from the COVID-19 Omicron variant eased late January into February, the upward pressure on rates slowly began to pull back. In March, volumes and rejection rates began to decline rapidly, and linehaul rates followed suit, giving shippers relief for the first time in 2 years.

Truckload Rates

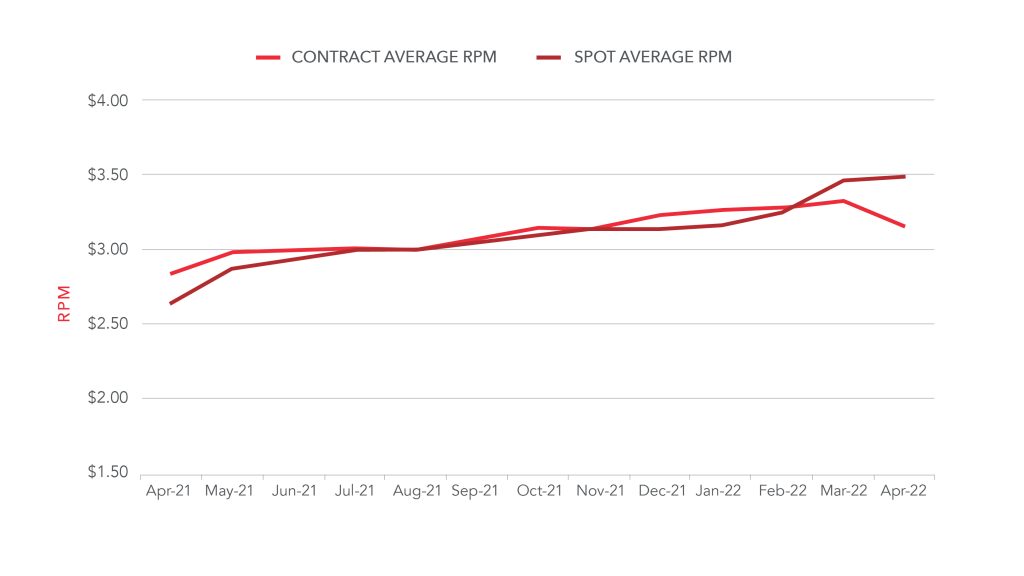

Using spot and contract data from DAT, FWF aggregated the monthly and quarterly rate-per-mile for reefers, flatbeds, and dry vans to determine the average rate-per-mile for the three trailer types combined.

|

Quarterly Contract RPM Including Fuel |

Quarterly Spot RPM Including Fuel |

|||||

| Quarter Average | RPM | % Change | Quarter Average | RPM | % Change | |

| Q3 2020 Average | $2.35 | Q3 2020 Average | $2.31 | |||

| Q4 2020 Average | $2.49 | +5.96% | Q4 2020 Average | $2.52 | +9.09% | |

| Q1 2021 Average | $2.65 | +6.04% | Q1 2021 Average | $2.62 | +3.96% | |

| Q2 2021 Average | $2.86 | +7.92% | Q2 2021 Average | $2.93 | +11.83% | |

| Q3 2021 Average | $3.01 | +5.24% | Q3 2021 Average | $3.02 | +3.07% | |

| Q4 2021 Average | $3.12 | +3.65% | Q4 2021 Average | $3.17 | +4.97% | |

| Q1 2022 Average | $3.29 | +5.45% | Q1 2022 Average | $3.28 | +3.47% | |

You can find the most up-to-date RPM data by trailer type on DAT.

During the first quarter of the year, contracts are negotiated with carriers and shippers looking to the spot market to determine fair contract rates. This typically leads to a decrease in spot rates and spot market activity, which was observed later than expected this quarter. Volumes and rejection rates fell rapidly at the end of Q1, which resulted in an overall decrease in spot rates.

This chart was created by FWF using aggregated RPM data from DAT.

Capacity typically gets tighter in March as activity and demand increase at the end of the quarter; however, this year was unseasonably soft and has raised concerns of a downturn in the freight market. COVID-19 related issues seemed to take a back seat as the decline of outbound volumes and rejection rates have picked up pace. Shippers saw very low tender rejection for the first time in two years, and they are learning that the market is turning in their favor as capacity loosens. Spot linehaul rates declined, though all-in rates were offset by the rapid increase of the cost of fuel, and equipment posts increased as March saw the largest number of new trucks entering the market.

Current Factors Driving the Freight Market

Diesel Prices

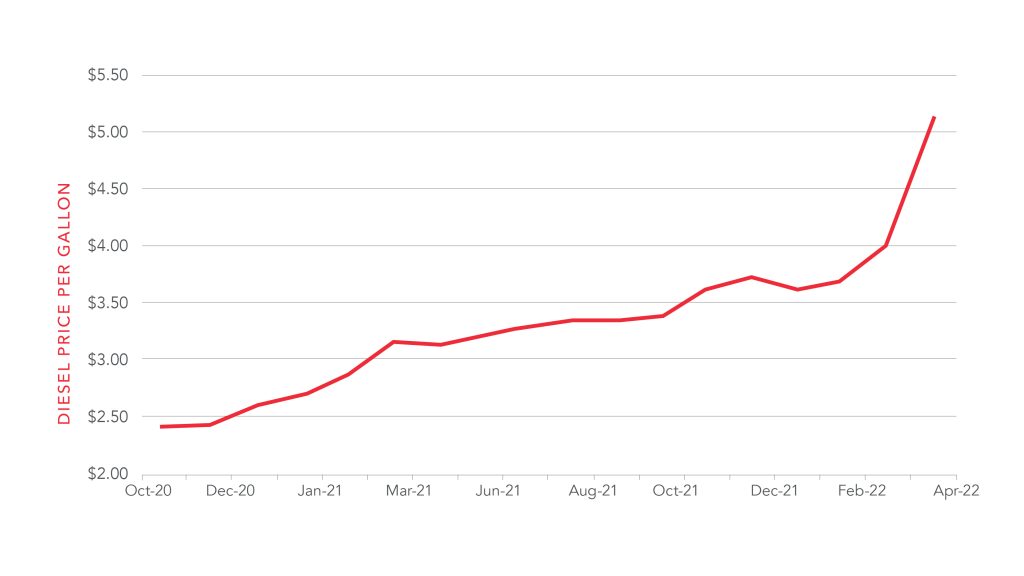

Diesel prices are a key factor in determining rates, and the average cost per gallon increased significantly in Q1. The EIA forecasted an increase in fuel in 2022 as demand would likely increase with the improvement of COVID-19. Along with the increase in demand, the Russia-Ukraine War also put upward pressure on the cost of fuel, with the average cost of diesel per gallon increasing 26.6% m/m in just March alone.

This chart was created by FWF using diesel price data from the U.S. Energy Information Administration.

Russia-Ukraine War

Although the freight market is cooling off, several market conditions are disrupting supply chains and causing continued shortages. The Russia-Ukraine War imposes a threat on global supply chains with possible long-lasting effects. Both Russia and Ukraine are exporters of many important commodities, including wheat, and are key producers of oil and neon. The impact that this conflict has on fuel has already made itself apparent at the pump, as the cost of fuel is expected to remain high through 2022.

Along with oil, almost half of the world’s neon and palladium supply used to make semiconductor chips is produced in Russia and Ukraine. The microchip shortage persisted through 2021, halting new trucks from entering the market and nearly doubling the cost of used Class 8 trucks. Bloomberg reported that the lag between when a chip is ordered and delivered reached a new high in March after slightly improving at the end of 2021.

China’s COVID-19 Lockdown

More supply chain concerns have been growing while COVID-19 spreads rapidly through China as several cities that are important global production and shipping centers have been in lockdown in attempts to contain the spread. Most factories and warehouses in Shanghai, the world’s largest port, are completely shut down as workers are stuck at home. Logistics companies in the area say that truck drivers are not permitted to go to other cities to move goods. Drivers also had to provide a negative COVID test and a special permit that expired every 24 hours to operate, causing massive traffic jams and wait times of up to 40 hours at highway entrances.

FreightWaves experts believe the damage that these lockdowns will have on the supply chain is comparable to the manufacturing blackout that began in Wuhan at the start of the pandemic two years ago. 82% of American manufacturers have already reported slowed or reduced production and 86% reported supply chain disruptions.

According to SONAR, container volumes out of Chinese ports began to drop at the beginning of April and have declined by more than 31%, suggesting less volume will enter the U.S. freight networks and further hinder the market. The longer China stays in strict lockdown, the greater the shockwave on the U.S. supply chain, though Chinese officials recently issued new guidelines in an attempt to ease supply chain issues. It is unclear if there will be short-term logistics relief.

Consumer Demand and Inflation

Due to the pandemic, consumer spending and demand reached unprecedented highs over the past two years. In response, retailers continued to order a large number of goods to meet this demand and even ordered extra to avoid supply chain issues and shortages. Last quarter, consumer demand eased as inflationary pressures fell onto consumers, while retailers continued to increase their inventories. This has created a bullwhip effect, and goods have nowhere to go as warehouse space is slim, and consumers are spending less, leading to slowed freight demand.

The Bureau of Labor Statistics reported that the Consumer Price Index increased 1.2% in March on a seasonally adjusted basis, after rising 0.8% in February, to 8.5% for the 12 months ending in March – the largest 12-month increase since 1981. As inflation remains elevated, consumer demand will continue to decrease and in turn, slow freight demand.

Despite a great deal of inflationary pressure on businesses and consumers, the U.S. economy is still growing. PMI measures 58.8, and any measure above 50 indicates an expansion of the manufacturing sector compared to the previous months. Consumers have been returning to work and FRED reported that the jobless claims report reached its lowest level since 1969, after peaking in April of 2020.

FRED also reported that the number of single-family homes under construction is at its highest level since 2006, while new and privately-owned housing remains elevated as the measure has continued to grow since the start of the pandemic. The demand for housing and construction increases the demand for flatbed shipping.

Conclusion and Q2 2022 Projections

The second quarter of 2022 is expected to remain positive, just not as robust as 2021. The 2021 freight market was far from the norm and is a difficult year to use in comparison, so year-over-year downturns are expected. While the dry van and reefer sectors are experiencing a decrease in demand, the produce season has officially begun, increasing reefer activity and putting upward pressure on rates through the Fourth of July. Flatbed demand is expected to remain high with upcoming volume from the $1T infrastructure bill and housing/construction markets as warm weather rolls in.

FWF continues to provide customers and carriers with reliable and new information to navigate the freight market with in-depth knowledge and data. Visit FWF’s resource center for more information that can improve your insights.